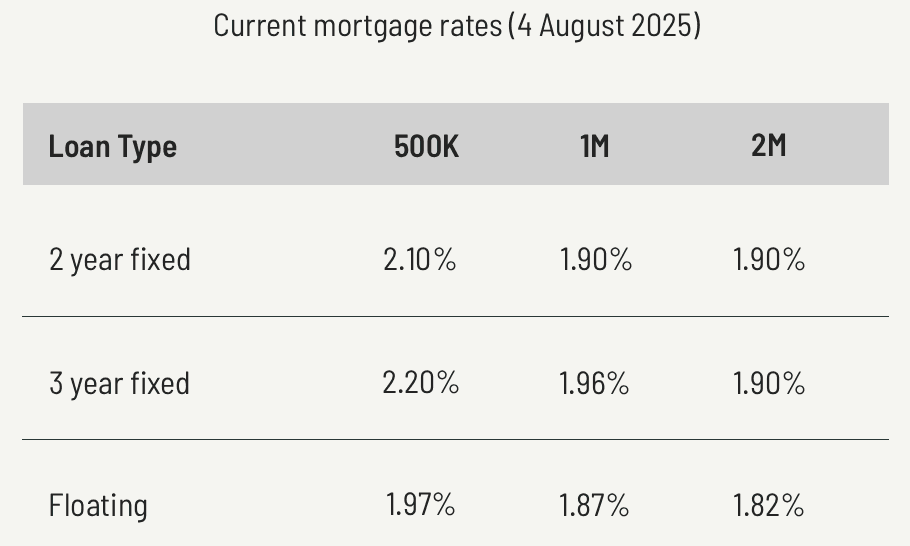

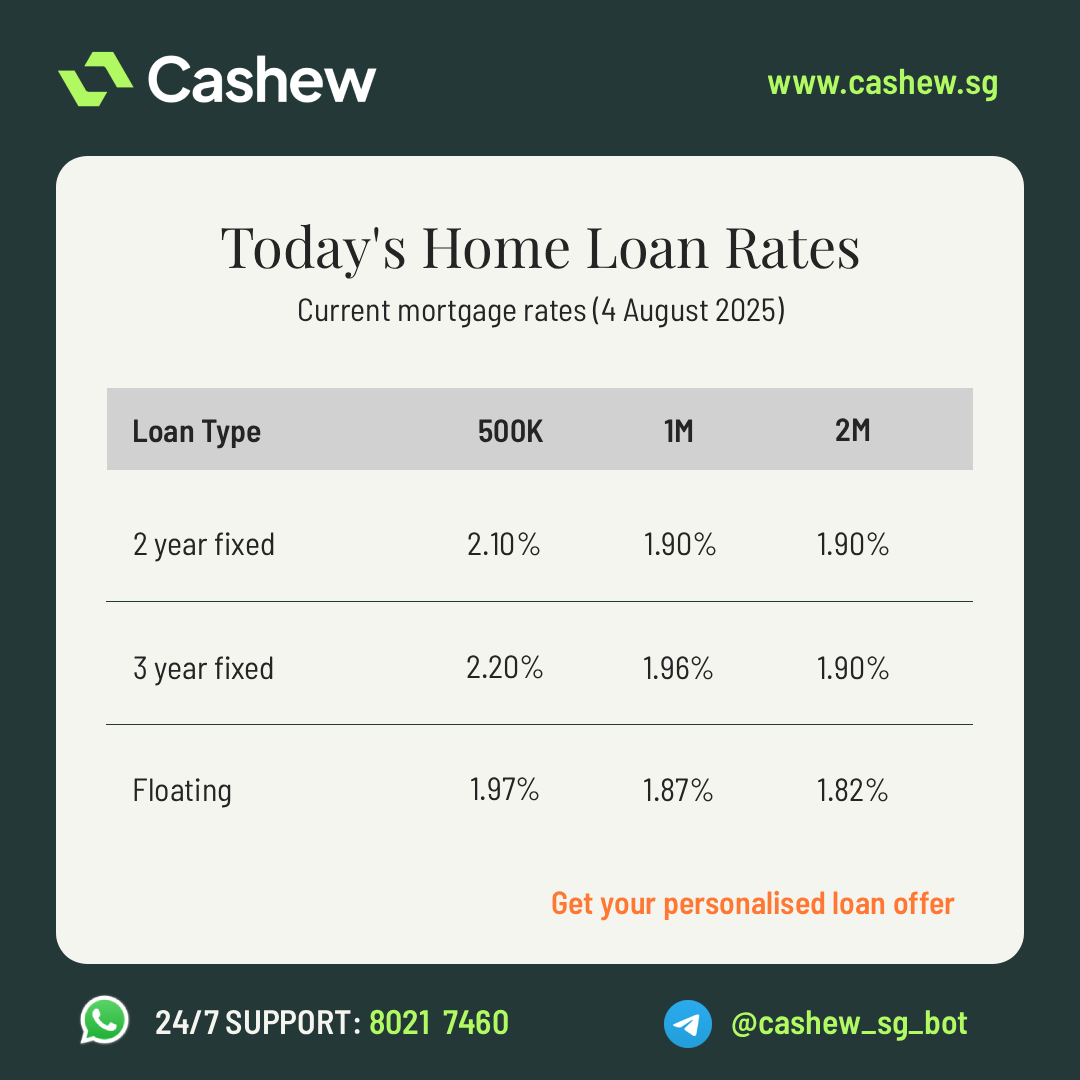

Singapore’s latest mortgage offers are drifting further south of the 2% mark, especially for loans above SGD 1 million. Analysts expect rates to stay around that level for the next couple of quarters - but they don’t see rates crashing back to the ultra-low levels of the 2010s any time soon.

Singapore’s benchmark 3-month compounded SORA has been on a broad-based easing path since early 2025, falling from a 3.66 % peak in mid-2024 to 1.85 % on 1 August 2025. The pull-back reflects cooler core inflation, a pause in Monetary Authority of Singapore (MAS) tightening, and a looming global rate-cut cycle.

With funding costs sliding, banks have trimmed mortgage pricing; headline packages now “hover around 2%,” and selected high-ticket loans have dipped under that threshold.

A quick sense check: the 1-month compounded SORA has been range-bound between 1.56 % and 1.68 % since mid-July, giving lenders ample room to keep promotional spreads razor-thin.

Consensus view: Most bank economists place 3-month SORA in the 1.8 – 2.0 % corridor through the year-end, slipping to about 1.6 % by mid-2026.

Beyond 2026: Econometric models point to ~1 % in 2026 and ~1.5 % in 2027—a gentle glide lower, but still above the sub-1 % in the 2010s.

In short, the market is pricing stability, not a free-fall: rates are unlikely to revisit the rock-bottom environment that prevailed before 2015, yet they’re also not expected to rebound sharply in the near term.

**Buying soon: **Locking in a fixed-rate below 2 % offers predictable payments at multi-year lows.

**Refinancing: **Even a 30 bp saving on a SGD 700k balance can cut interest costs by ~SGD 2,100 per year.

**Waiting on the sidelines: **Forecasts suggest no dramatic drop ahead—holding out for 1 % could mean missing today’s sweet spot.

Have questions about which offer fits your profile? Reach out to Cashew’s advisors or start an instant chat on WhatsApp.

© 2026 Cashew. All rights reserved.